While there is much uncertainty about the outlook for standard-essential patent royalty rates in court determinations, there are plenty of solid benchmarks in well-established comparable licenses (“comps”). The former rates are thin on the ground and have been made up based on some dubious and fiercely contested tenets as judges scrabble to set figures that are fair, reasonable and on-discriminatory. The latter rates have been agreed in droves through negotiation in licensing programs with dozens of licensors, hundreds of licensees and many thousands of patents. These are not meaningless asking prices with no takers —or just one or two transactions specifically conceived and executed to establish a desired marker— they are economically significant because they are underpinned by many billions of dollars of licensing trade over decades.

And, many players in the cellular industry have self-servingly colluded to cap aggregate royalties since the introduction of 3G twenty years ago. Unsurprisingly, these voices dominate because most, by far, of the interested parties, including OEMs, must become licensees to implement the standards legally. For only a few is licensing more an income generator than a cost in manufacturing.

And, many players in the cellular industry have self-servingly colluded to cap aggregate royalties since the introduction of 3G twenty years ago. Unsurprisingly, these voices dominate because most, by far, of the interested parties, including OEMs, must become licensees to implement the standards legally. For only a few is licensing more an income generator than a cost in manufacturing.

Who is to say how much all the patents in devices are worth, how that valuation should be derived and how value should be divided among technology owners, implementers and end users? Weighing up all of this is significantly a matter of personal judgment—not of simply applying some supposedly pre-ordained formula. Vacating the District Court Judge Selna’s bench trial decision in TCL v. Ericsson on appeal, the Federal Circuit has prescribed retrial with a jury. This will recalibrate awards based on the subjective judgement of randomly selected non-experts. It will likely include consideration of bottom-up valuation methodologies reflecting consumers’ purchasing preferences, price sensitivities and the perceived value for smartphone features and performance improvements.

The math(s) is not easy or proven

Even using comps is not straightforward in many cases because most licenses are cross licenses and so the prices and monies paid typically reflect significant netting off between the notional royalty rates of the parties and also account for the respective trading flows of their manufactures. Where licensors do not have downstream manufacturing businesses, that need licensing—such as smartphone manufacturing—royalty rates can more easily be directly compared among licensees, in many cases, without adjustment. For example, Qualcomm and InterDigital do not make or sell devices, which account for most, by far, of the trading value in the cellular products (e.g. around $500 billion per year for mobile phones). Adjustments are also required in the comparison of licenses due to up-front lump sum payments, per-device caps, per device floors, total payment caps and other differences.

So how on earth could something as seemingly complex and difficult as valuing a portfolio of SEPs be left to a bunch of jurors? Judge Selna’s decision was extensive and 115 pages long. It applied two different methodologies —"top down” and “comparable license analysis” with the “unpacking” of two-way licenses—and disregarded a third—a bottom up “Ex Standard approach” designed to estimate the value of SEPs independent of any value arising from incorporation of SEPs into a standard. With his judgement vacated, Judge Selna’s analysis no longer has any legal authority; but it does reveal some of the methods and arguments that may continue to be applied in the valuation of SEPs and determination of royalties for these under FRAND terms.

The wisdom of lay folk

Perhaps the jurors will see through all the bluff and complexities, as they do in so many other trials. They can be unburdened by the weight of consensus, self-interested majorities and conventional wisdom. The Seventh Amendment constitutional right to a jury trial in civil proceedings has served the US well. It is probably one of the reasons why the nation is for centuries the most successful technological innovator in the world. If not, the US has evidently not been held back by its patent law and execution of this right.

Significantly, the New [December 2019] Policy Statement on Remedies for Standards-Essential Patents Subject to Voluntary F/RAND Commitments issued by The U.S. Patent & Trademark Office (USPTO), the National Institute of Standards and Technology (NIST), and the U.S. Department of Justice, Antitrust Division (DOJ) offers views on remedies for standards-essential patents that are subject to a RAND or FRAND licensing commitment. This overturns interpretations of the 2013 policy statement by the USPTO and DOJ: ‘the agencies have heard concerns that the 2013 policy statement has been misinterpreted to suggest that a unique set of legal rules should be applied in disputes concerning patents subject to a F/RAND commitment that are essential to standards.’ In addition to saying a lot about how injunctions should become more readily available—an important issue, but which is outside the scope of my article— the new Policy Statement advises that ‘with respect to damages, the Federal Circuit has explained, “We believe it unwise to create a new set of Georgia-Pacific-like factors for all cases involving RAND-encumbered patents.” The court further stated that “[a]lthough we recognize the desire for bright line rules and the need for district courts to start somewhere, courts must consider the facts of record when instructing the jury and should avoid rote reference to any particular damages formula.”’ (Emphasis added and citations omitted.)

With the above developments, we are likely to see rather higher awards for SEPs than, for example, the paltry figure of somewhat less than one US cent per LTE SEP resulting from Judge Selna’s overturned decision.[1]

Juries tend to award rather larger damages figures. In Qualcomm v. Apple, San Diego, March 2019, the figure of $1.41 per iPhone was awarded for infringement of three non-SEPs (i.e. 47 cents per US patent. A Los Angeles jury just awarded the California Institute of Technology (Caltech) $838 million from Apple and $270 million from Broadcom—totalling approximately $1.1 billion—for infringement of four patents used in the implementation of the WiFi standard (IEEE 802.11). Per device, this is equivalent to $1.40 (35 cents per patent) for Apple and 26 cents (6.5 cents per patent) for Broadcom.

Three different portfolio valuation and FRAND determination methods where presented by the parties for Ericsson’s 2G, 3G and 4G SEPs in TCL v. Ericsson.

“Reasonable, maximum aggregate royalties” with “proportionality”

I have already criticized at length Judge Selna’s top-down approach and so I provide no more than a summary of that here. When I wrote my critique of Judge Selna’s subsequently vacated Decision, I focused almost entirely on his top-down analysis; but indicated I might return to assess the other methods of FRAND rate determination and his analysis of them.

Top-down is fundamentally flawed for two reasons, and thirdly, Judge Selna’s corresponding determinations were biased and erroneous in his application of the methodology.

Firstly, the selected aggregate royalty rate caps—of 6 to 10 percent for 4G LTE and 5 percent for 3G— do not reflect the value of the underlying technologies. The figures are quite arbitrary and were only advocated by those who wanted to limit royalties to those levels. Why should the value of IP versus hardware in a smartphone be limited to such small percentages of its purchase price when the corresponding percentages for IP in music CDs, video DVDs, software CD ROMs or patented pharmaceuticals are more like 80 percent?

Judge Selna justified use of this approach on the basis that Ericsson and others had in 2008 encouraged the industry to allocate royalties based on a maximum aggregate rate and proportionality among licensors based on relative patent strength among portfolios. However, there were several in the industry that never subscribed to such an approach and were, instead, for good reasons, vociferously opposed to it. For example, in December 2008, Qualcomm publicly stated it was against such a formulaic approach because it ‘would arbitrarily limit the value of standards essential patents, discourage innovation, encourage the filing of marginal patents, complicate and delay the standardization process, and be impossible to implement in practice.’ There is no reason to bind these dissenters to such an approach. It should be possible for them and others to derive significantly higher royalties, if enough value is there.

Secondly, apportionments among patent holders are inaccurate. For example, patent-portfolio stand-essentiality determinations are cursory, inconsistent and patent counting methods typically assume all patents are of equal value, which is antithetical to valuation principles in patent law. Counting technical contributions to standard-setting organizations also has the shortcoming of rewarding quantity instead of quality.

Thirdly, Judge Selna erroneously whittled the rates down for Ericsson in several ways:

- Regarding company and aggregate single-mode rates as multimode rates,

- Using inaccurate, unreliable and likely biased patent assessments in apportionment of the aggregate rate to Ericsson with:

- inflated patent counts in the denominator,

- deflated patent counts in the numerator,

- Regarding announced rates, including aggregate rates, as US rates rather than global rates,

- Discounting indicated rates based on patent expirations, even though indicated rates were based on certain expectations for these expirations,

- Disregarding the value of standard-essential improvements and Ericsson’s share of these.

While the cap is purportedly to protect implementers from the “worst case” scenario with a “royalty stack;” in fact, nobody pays anywhere the maximum figure. On average, as I have shown and as others have confirmed, here and here, the aggregate royalty paid on mobile phones including smartphones is no more than around 5 percent including all generations of cellular SEPs, non-cellular SEPs and non-SEPs. That is net of cross-licensing, but even those with nothing to cross license are not paying much more. For example, TCL managed to hold out payment to Ericsson for 7 years before trial. There was no evidence presented in that case that TCL was paying anywhere near or above an aggregate of 10 percent, nor that it would be doing so with payment to Ericsson at the rates set in Judge Selna’s Decision. I have never seen evidence that anyone has paid an aggregate figure reaching or even approaching 10 percent for LTE licensing.

Fair shares for all

While the value created in an invention can be enormous, this is shared among various participants in the value chain. Ultimately, virtually all the benefits tend to flow downstream to end users. In the interim, some of the value is rightly captured in profits by technology developers, OEMs and service providers.

Judge Selna threw out the “Ex Standard” valuation methodology of Ericsson’s expert David Kennedy because, in Selna’s opinion, the values it derived were too high:

‘Ericsson's 4G Essential Patents confer $6.15 to $7.14 of value on a 4G handset. The Court finds that Kennedy's result are highly suggestive of royalty stacking; i.e, valuing individual components of a standard in manner that accedes the aggregate value of the standard.’

He also wrote: ‘it is simply not logical that two features could have a value in excess of Ericsson's entire portfolio.’

These statements confuse the concept of value to the user with the technology-licensing price to an OEM that is fair and reasonable or that would be negotiated commercially under market conditions. The above figures represent maxima — not figures demanded, let alone expected or likely to be anywhere near realised by licensors.

Consumer surplus is defined as the difference between the consumers’ willingness to pay for a good and the amount that they actually pay. On average, producers capture only small percentages of the total welfare gains from innovation, with consumers capturing the remaining surplus. Licensing rates determine how the licensors and licensees split the producers’ share of those total welfare gains.

The FRAND rate licensing price reflects two factors:

Value to consumer ($) x share of value to be accrued by licensor (%) = royalty to licensor ($).

Bottom-up valuation methods, including Ericsson’s Ex Standard approach derive an upper limit to what features are worth. What licensors may yield from them in licensing fees is a question of rent splitting and how the economic surplus is shared among licensors, their licensees and downstream parties including mobile operators, over-the-top service providers (e.g. Google, Facebook and Netflix) and end users.

Economics and market dynamics tend to determine outcomes including how economic surpluses are shared. For example, while research has shown that the value a consumer derives from Google search may be tens of thousands of dollars per year per user, Google is happily making huge profits while generating, only, hundreds of dollars per person. Hypothetical choice experiments can derive consumer values, even for services such as Google that have zero pricing for consumers. Internet platforms—such as Google— are under intense scrutiny by competition authorities due to their dominance and how they might be abusing that rather than for their high profits per se. In litigation, such as in TCL v. Ericsson, jurors must decide how much of the large economic surpluses generated by SEP technologies are awarded in licensing fees.

Get (un)packing

While comparable licenses are potentially the very best valuation benchmarks because they reflect billions of dollars of trade with many licensing agreements over many years, not all of these can be employed directly before significant adjustments. Lump sum payments, differences between sales forecasts (most applicable because the assumption is that licenses should have been completed before trading) and actual sales (20:20 hindsight), and assumed “net present value” discount rates can all have significant effects on derivation of simple, one-way licensing rates from complex two-way licensing agreements including multiple terms and conditions.

I also explained the complexities and difficulties of “unpacking” comparable licenses to derive the effective one-way licensing rates in another article I published last year. One of the issues I discussed there is that licensing rates tend not always to be proportional to the number of patents— as assumed by both parties’ experts in TCL v. Ericsson—in unpacking Ericsson’s cross licenses to derive simple “one-way” licensing rates. Among many examples of that phenomenon, is IBM’s historic licensing approach, with pronounced non-linearity in licensing fees for more than five patents:

| Number of Licensed Patents Covering the Product |

Percentage of the Selling Price |

| 1 |

1% |

| 2 |

2% |

| 3 |

3% |

| 4 |

4% |

| 5 or more |

5% |

Bottoms up

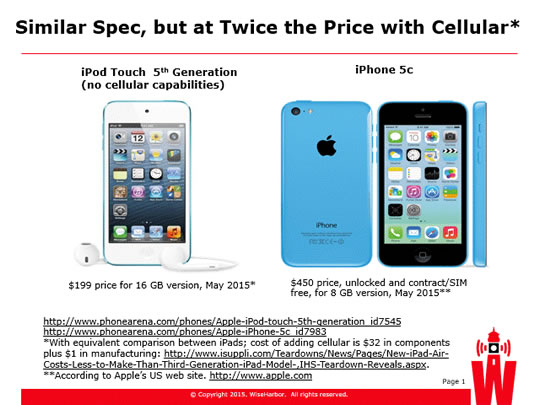

In a presentation I gave on the topic of top down and bottom up valuation methodologies at the Patents in Telecoms and the Internet of Things conference at Tokyo University in November 2019, I reused some analysis I have been presenting since 2015 showing how cellular functionality is priced by Apple at a much higher mark-up than other costs. Apart from the absence of cellular capabilities, the iPhone Touch 5th Generation had very similar specifications to the iPhone 5c. However, the latter was sold for $450, which was more than twice the price of the former, despite costing only around $32 more in manufacturing.

Even more remarkable from an economic perspective was the fact that sales volumes for iPhones in 2014 were more than 12 times greater volume terms and 46 times greater in revenue terms than for all iPods. Apple is free to price at any level it wishes and so its prices are only an indirect indicator of consumers’ perceptions of value. Relative sales performance is an outcome of its pricing. According to basic economic principles, if two products are close substitutes a much lower price for one would tend to result in much greater demand for versus the other product. The much higher demand for the cellular devices— despite the much higher price— underlines the premium value in cellular and that no iPods are close substitutes for iPhones.

Out on the Range

FRAND rates are not as range bound or unique, as many might imagine they should be. It all depends on the circumstances, other licensing terms and market developments over the years. On appeal, Justice Birss’ Decision in Unwired Planet v. Huawei was largely upheld and partially annulled. The higher court ruled several different sets of rates and terms could all be FRAND and that there did not have to be only a single FRAND rate, as Birss had ruled.[2]

I have been arguing here since 2013 that the FRAND rate range should be quite wide because, for example, patent pool participants legitimately tend to agree on relatively low rates in the interests of their downstream-oriented members versus legitimately agreed bilateral FRAND rates. I have not yet come across anyone arguing that royalty-free patent pools or “platforms”, such as that for the Bluetooth and USB standards, have rates that are non FRAND. Common sense suggests that royalty free is not an isolated incidence of what is FRAND where other licensing arrangements set a significant non-zero FRAND rate. The range of rates that are FRAND must at least span between these figures, subject to other licensing terms and conditions.

In my abovementioned Tokyo presentation, I also showed that FRAND rates for video codecs have varied enormously over time and between competing patent pools. It is remarkable that the maximum licensing cost (set in dollars rather than as a percentage of the product selling price) for the MPEG 2 standard technology pool was 10 times higher than the 20 cents maximum for its higher-performing successor MPEG 4 (AVC/H.264)—even over the years in which use of the two standards was substantially overlapping. Many commercial factors were at play, including the fact that the latter standard was adopted in much higher volumes by being software based rather than hardware based and being used mostly in smartphones rather than in the domestic CE products including TVs, set top boxes and DVDs into which MPEG 2 was primary introduced.

Have we had enough of experts?

As a testifying expert witness, I would be one of the last to propose getting rid of them: but none of them, nor their sponsors or acolytes, nor those who are swayed by them have a monopoly on wisdom or are infallible. Following those with prevailing views is a safe bet for those in the firing line of scrutiny with tricky and contentious decisions to make. But that does not make those views right. Bias towards consensus or the majority is not justice. As the New Policy Statement identifies, courts have misguidedly tended to follow a unique set of rules in dealing with FRAND disputes.

On account of it finally being Brexit Day, today, it is most fitting to paraphrase British Member of Parliament and outspoken Brexiteer Michael Gove—who maintains he was misrepresented when it was reported he had said ‘people have had enough of experts’ in the highly contentious debate about the merits and costs of Brexit. Rather than do away with experts, one should always look for the dissenting voice. When there appears to be a settled consensus, look at the people who are challenging it. If their arguments are well constructed, then pay close attention; if you think it is just bogus nonsense then reject it— but test alternative propositions. The notion that things should be taken simply on trust because of someone’s position is an invitation to intellectual conformity and what we need is a vigorous, debating, dissenting culture.

On account of it finally being Brexit Day, today, it is most fitting to paraphrase British Member of Parliament and outspoken Brexiteer Michael Gove—who maintains he was misrepresented when it was reported he had said ‘people have had enough of experts’ in the highly contentious debate about the merits and costs of Brexit. Rather than do away with experts, one should always look for the dissenting voice. When there appears to be a settled consensus, look at the people who are challenging it. If their arguments are well constructed, then pay close attention; if you think it is just bogus nonsense then reject it— but test alternative propositions. The notion that things should be taken simply on trust because of someone’s position is an invitation to intellectual conformity and what we need is a vigorous, debating, dissenting culture.

While all but a relatively small proportion of SEP portfolio licenses are negotiated to completion between or among parties, it is time for some fresh thinking and judgement on where value lies and how it should be shared when there is dispute. I am looking forward to seeing what jurors will come up with.

[1] A figure of 0.5 cents per SEP can be calculated by dividing Judge Selna’s 0.45% LTE royalty rate award by the figure of 125 patents declared essential and claim charted by Ericsson and then multiplying that figure by the approximate average selling price of $140 per LTE handset manufactured and sold by TCL in the relevant period from 2013 to 2015. The calculated figure increases to 0.9 cents if, as TCL’s Expert Dr Kakaes opined, only 70 of Ericsson’s patents are deemed standard-essential to LTE.

[2] As noted by Herbert Smith Freehills ‘One of the few points on which the Court of Appeal disagreed with Birss J was on the question of whether there can only ever be a single set of FRAND terms as between a potential licensor and licensee, as the judge had found at first instance. The Court of Appeal were of the view that it was ‘unreal’ to think that two parties will necessarily arrive at precisely the same set of terms as two other parties (all of them acting fairly and reasonably and faced with the same set of circumstances). Rather, the Court of Appeal held that a number of sets of terms may all be fair and reasonable in a given set of circumstances, finding that this approach was supported by the economic evidence.’